from CMATT

-------------------------------------------

OK now for my opinion on AAPL

there are many reasons i'm so bullish on AAPL, but I will just mention the main 2

#1 is valuation,and this what affects my opinion in the short term I feel the valuation on AAPL is way off at this time, I felt that way before the recent devalue in the PPS, which IMO was due to some funds who were short Read More...

Friday, December 29, 2006

Tom Preston: Trading resolutions for 2007

This is a transcript from a session Tom Preston at Thinkorswim did a few days ago. When TOS posts this transcript on Chat Archive I will remove this post. Mean while I felt this was soooo good that I post here in advance for anyone that misssed the session.

----------------------------------------------------------------------------------------------------------

Tom Preston: Trading resolutions for 2007

Tom Preston: 1) Don’t try to make back all your losses in one trade

Everyone makes losing trades. Sometimes you get the losers in a row, one after the other, and your account is smaller than when you started. You get frustrated and angry. You decide to take revenge on the market and make all your losses back and then some. So, the next trade you make, you increase the number of contracts or shares because your rage is overpowering your discipline and you’re sure that this trade will be “the one”.

And…you’re probably wrong. The trade turns out to be loser as well and your account is even deeper in the hole. Sure, it might be a winner, but it’s not worth the risk. Don’t let your anger control your trading. Just because you’ve had a string of losers doesn’t necessarily mean your due for a winner.

If you’re in the situation of having nothing but losing trades, a better idea would be to review your trading plan and see if there might be fundamentally wrong with it. Then you can correct it and see if that improves the results.

Tom Preston: 2) Don’t take stupid risk

This goes along with the first resolution. The bottom line is, don’t put your hard-earned money at risk unless you have a good reason to do so. To spin the old trading adage a little differently, if you have a hunch, DON’T bet a bunch. Keep your risk under control.

We suggest that you keep the max risk of any one trade to less than 5% of your trading capital. And keep the total risk of all your open positions to less than 25% or so of your trading capital. That means, if everything goes wrong, you won’t lose everything, and you’ll still have some money left to continue trading.

Also, having some kind of trading plan in place that gives you some consistent criteria for entering and exiting positions will help you put the trades you make based on “gut” feelings or something outside of those criteria in perspective. You can put those trades on, just don’t risk any more on them than you would your “criteria-based” trades, and maybe even less.

Tom Preston: 3) If it looks too good to be true, it is

I can’t stress this enough. I have been saying this since I started thinkorswim, and I find myself saying it again today. Option prices are not wrong. Now, I’m not talking about errors in the quote database. That’s a technical problem. What I mean is that if you see a box spread trading over the difference between the strikes, or a calendar spread trading for a credit, or an adjusted option trading for more than an unadjusted option on the same stock, with the same expiration and strike price, money is NOT lying on the floor just waiting to be picked up. Rather, it means that there is something else impacting those option prices like a dividend or something that you don’t see, but the pros do. The pros are right. It is a fact of the state of option trading that there are no arbitrage opportunities sitting there waiting for the retail traders (you) to take advantage of them.

Tom Preston: 4) Use spreads whenever possible

If you are trading directionally, that is, you are betting on a stock or index going up or down and you want to use options, please consider using verticals. Lately, I’ve been seeing a lot of customers betting on the direction of stocks or indices using simple long calls or puts. Now, I don’t have a problem with directional trading in and of itself. But long single options have sensitivities to time decay and volatility that can make a losing trade out of one that is right on direction. And if you’re buying in the money options, they usually have wide bid/ask spreads and can be less liquid than at the money or out of the money options, so that if you want to/have to exit the trade, you get lousy execution prices.

Verticals are great for when you are less than 100% confident that the stock or index will go in the direction you think it will. If you’re bullish, consider selling an out of the money put vertical. You make money if the index goes up, stays the same, or maybe even drops a little. If you’re bearish, consider selling an out of the money call vertical. Short verticals have positive time decay and less vega sensitivity than outright long options. Yes, their profit potential is less, but so too can be their max loss. If you don’t do too many of them (remember our suggestion of not risking more than 5% on any one trade?) they’re a good way of keeping risk under control.

Tom Preston: 5) Keep learning

Don’t stop trying to learn new things about trading, either by doing research, reading books and articles, coming to classes (try www.optionplanet.com), joining us here on Wednesday afternoons, calling the TOS trade desk with questions, etc, etc.

Everyone is getting smarter and more capable. The tools that we give you for free are more powerful than what I was using when I was trading professionally. You can learn things here no retail trader would have known certainly 20 and maybe even 5 years ago. The difference between the educated retail trader and the professional trader is getting smaller and smaller. That’s both good and bad for you. It’s good that bid/ask spreads are tighter now than they have ever been. You can see live quotes for free. But it also means that the industry is more competitive. Knowing what an iron condor is or how to calculate a roll value isn’t enough. There are hundreds of TOS customers who already know that stuff already. Making money trading is very hard work. You have to be willing to devote the time and energy to try to find an approach to trading that might actually make you money. A successful trading career isn’t built out of luck.

Wednesday, December 27, 2006

Sell your vested employee stock options!!!!!

Imagine u worked for a firm that granted you a s*** load of options that have become fully vested. Unfortunately for the time being they are under water. A pile of worthless paper? Maybe not for long!!!!!

Jadedbear from #options once related an attempt to low ball purchase employee stock options for cheap. Theoretically these non transferable options have ample time value left, even the under water ones. His attempt was unsuccessful but was an interesting idea. Soon, however, this may all change, starting with Google. Check out the skinny originally from The Wall Street Journal.

Jadedbear from #options once related an attempt to low ball purchase employee stock options for cheap. Theoretically these non transferable options have ample time value left, even the under water ones. His attempt was unsuccessful but was an interesting idea. Soon, however, this may all change, starting with Google. Check out the skinny originally from The Wall Street Journal.

Thursday, December 21, 2006

ICE position comparison

This post will demonstrate how a synthetic collar can be substituted with a simple diagonal spread, with less transaction costs. I saw this collar talked about in Woodiescciclub.com

------------------------------------------------------------------------------------------------

Synthetic collar.

+Mar 110c

+Mar 110c

- Mar 110p

+Mar 105p

- Jan 115c

The 110c and 110p form synthetic long stock.

The synthetic long stock and the 105p form synthetic long call(with deductible). So essentially the position was deduced roughly down to:

+ March call

- Jan call

A long diagonal spread.

------------------------------------------------------------------------------------------------

Here is the equivalent long diagonal spread:

Here is the equivalent long diagonal spread:

+Mar 105c

- Jan 115c

debit 10.25

Only 2 legs to worry about, comparable greek risks, less commissions, less bid/ask spread to overcome, better breakeven point.

Debit is kinda high you said?

Compare its cousin using puts in the next position.

The ONLY difference in this position here compared to its "call" cousin above, its using puts, but essentially the same thing. Calls are puts, and puts are calls.

+ Mar 105p

- Jan 115p

credit .50

Which one of the three positions would you choose? ;-)

------------------------------------------------------------------------------------------------

Synthetic collar.

+Mar 110c

+Mar 110c- Mar 110p

+Mar 105p

- Jan 115c

The 110c and 110p form synthetic long stock.

The synthetic long stock and the 105p form synthetic long call(with deductible). So essentially the position was deduced roughly down to:

+ March call

- Jan call

A long diagonal spread.

------------------------------------------------------------------------------------------------

Here is the equivalent long diagonal spread:

Here is the equivalent long diagonal spread:+Mar 105c

- Jan 115c

debit 10.25

Only 2 legs to worry about, comparable greek risks, less commissions, less bid/ask spread to overcome, better breakeven point.

Debit is kinda high you said?

Compare its cousin using puts in the next position.

The ONLY difference in this position here compared to its "call" cousin above, its using puts, but essentially the same thing. Calls are puts, and puts are calls.

+ Mar 105p

- Jan 115p

credit .50

Which one of the three positions would you choose? ;-)

TELK position comparison

TELK - 17.11 (long) x 300

TELK - 17.11 (long) x 300jan 25c - 2.05 (short) x 3

jan 15p - 3.30 (long) x 2

Total debit (at 50% margin) $2800 tied up(in a retirement acct it will be $5k+)

If stock went to 10 by expiration lose $1175

If stock went to 5 by expiration lose $1650

Max absolue risk $2000+

Max gain above 25 = $2322

slightly short vega -1.79

ROI against max risk 116%

ROI against dough tied up 82%

ROI against risk at stock going to 10 = 197%

ROI against risk at stock going to 5 = 140%

ROI against risk at stock going to 0 = 116%

+jan 15c 3x -$510 ea.

+jan 15c 3x -$510 ea.-jan 25c 3x +$205 ea.

Total debit $915 amt of dough tied up

Max absolute risk $915

Max gain above 25 = $2085

flat vega risk

Max ROI against absolute risk 227%

ROI against dough tied up 227%

ROI against risk at stock going to 10 = 227%

ROI against risk at stock going to 5 = 227%

ROI against risk at stock going to 0 = 227%

Wednesday, December 20, 2006

Proprietary Trading audio archive posted

This post has expired, and the content removed at the request of the original producers of the archive, sorry. Expiration date 1/31/07.

Tuesday, December 19, 2006

How does delta and IV effect AGIX iron condor?

Just cut a video explaining how I see the effects are,

posted in the video section, named Delta+IV on iron condor.

posted in the video section, named Delta+IV on iron condor.

Saturday, December 16, 2006

Retail margin vs. Risk margin seminar archive now posted

It is now posted in the Learning video

area, hot off the press session I did a

few hours ago. Please check it out.

area, hot off the press session I did a

few hours ago. Please check it out.

Wednesday, December 13, 2006

Titanium Collar??

I posted the details in my new message board for discussion. It appears to be a way to protect long stock position thru news by turning it into a long straddle with very little additional cost.....

Monday, December 11, 2006

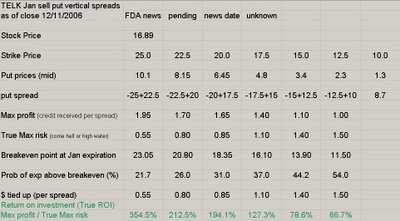

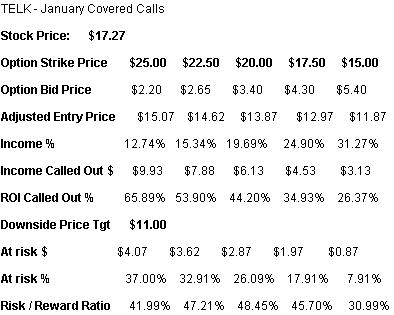

TELK FDA play covered call vs bull put spread

Andy from InvestorVillage proposes the following covered call table for consideration, on TELK. You can read the reasoning behind the numbers from Andy's post at InvestorVillage .

---------------------------------------------------------

Here is one of many alternative ways to skin the same cat. Click on pic to enlarge.

Comments welcome.

Sample order entry screen on Thinkorswim

---------------------------------------------------------

Here is one of many alternative ways to skin the same cat. Click on pic to enlarge.

Comments welcome.

Sample order entry screen on Thinkorswim

Saturday, December 09, 2006

Married put vs call video clip posted

This 6 minute video is now posted in the video section to the left.

It attempts to explain why long stock + put is really the same as long call of the same strike.

Your scrutiny is welcome.

It attempts to explain why long stock + put is really the same as long call of the same strike.

Your scrutiny is welcome.

Dan Sheridan CBOE webcast, a must see!!!

I have been watching Dan's free webcast series at the CBOE Learning Center and am plugging the series here.

The two topics that stand out the most in my mind (I am about 75% thru the series) are:

How to pick good calendar spared candidates and why large skews may be a bad thing?

How to creatively adjust your vanilla iron condors or butterflies? (in ways that I have never thought of before)

To pick up the rest of the golden nuggets......u will have to view the series yourself. Even if u are a seasoned trader, the guy is a riot to watch, he is a natural in front of the camera.

Registration is all free at the CBOE Learning Center.

Oh, if u see Dan ask him if I can get a free mentoring course for myself ;-)

The two topics that stand out the most in my mind (I am about 75% thru the series) are:

How to pick good calendar spared candidates and why large skews may be a bad thing?

How to creatively adjust your vanilla iron condors or butterflies? (in ways that I have never thought of before)

To pick up the rest of the golden nuggets......u will have to view the series yourself. Even if u are a seasoned trader, the guy is a riot to watch, he is a natural in front of the camera.

Registration is all free at the CBOE Learning Center.

Oh, if u see Dan ask him if I can get a free mentoring course for myself ;-)

Thursday, December 07, 2006

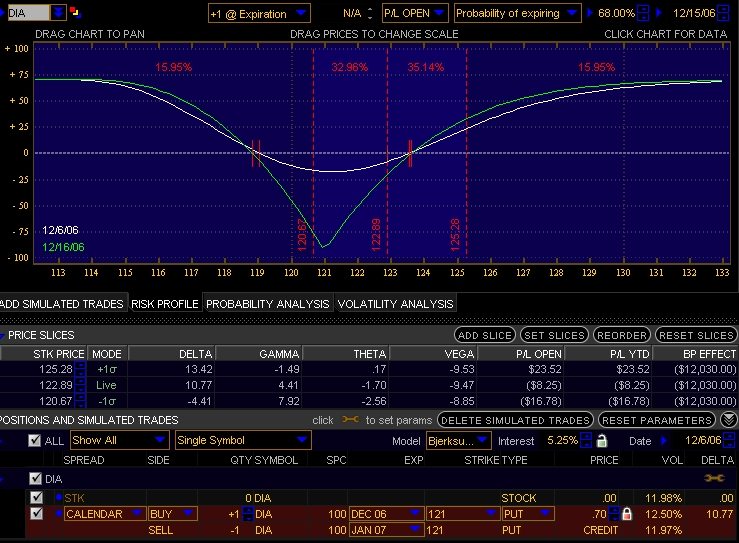

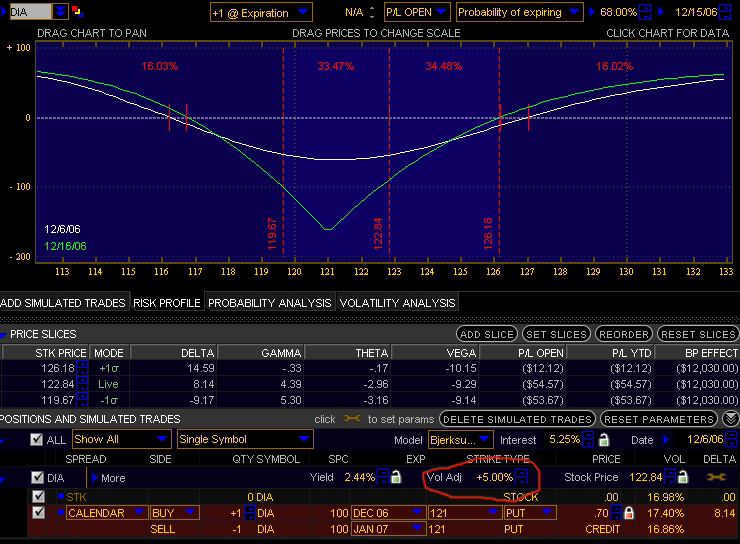

DIA Reverse Calendar example

Q:

my broker (www.thinkorswim.com) offers the possibility to view what

trades other customers enter and today (December 6th) someone entered

sell Jan 121 DIA put

buy Dec 121 DIA put

for a credit of 70 cents when DIA is at 123. Apart from the fact that

he might want to exit a position, let's assume he is opening this

position. Now I wonder, what is his rationale here?

In 10 days the December option is expired and he will be short the

January position. Anybody having an idea what this person is up to?

I guess if the market goes up, then he can buy back the short put

cheaper, but is that it?

thanks, gis

P.S. Many thanks to Ricky and options junky for answering my question

about the back ratio spread and the charts junky!!!

-------------------------------------------------------------

A:

Its quite possible, as others have pointed out, this could be a part of a larger order or a rolling order. But suppose its an order to open a lone position, this is the risk profile, note how much margin is required, why is that?

A seemingly low risk looking risk graph above with large margin requirement is partly due to its vega risk. When the position is short volatility, an increase in IV hurts the overall position. In theory there is no ceiling on how high IV can go, thus the large margin. The other risk to the clearing firm is when the front month expires and the retail trader does nothing to terminate or cover the short jan leg.

The graph below simulates a 5% increase in IV overall, note the max risk and breakeven now.

my broker (www.thinkorswim.com) offers the possibility to view what

trades other customers enter and today (December 6th) someone entered

sell Jan 121 DIA put

buy Dec 121 DIA put

for a credit of 70 cents when DIA is at 123. Apart from the fact that

he might want to exit a position, let's assume he is opening this

position. Now I wonder, what is his rationale here?

In 10 days the December option is expired and he will be short the

January position. Anybody having an idea what this person is up to?

I guess if the market goes up, then he can buy back the short put

cheaper, but is that it?

thanks, gis

P.S. Many thanks to Ricky and options junky for answering my question

about the back ratio spread and the charts junky!!!

-------------------------------------------------------------

A:

Its quite possible, as others have pointed out, this could be a part of a larger order or a rolling order. But suppose its an order to open a lone position, this is the risk profile, note how much margin is required, why is that?

A seemingly low risk looking risk graph above with large margin requirement is partly due to its vega risk. When the position is short volatility, an increase in IV hurts the overall position. In theory there is no ceiling on how high IV can go, thus the large margin. The other risk to the clearing firm is when the front month expires and the retail trader does nothing to terminate or cover the short jan leg.

The graph below simulates a 5% increase in IV overall, note the max risk and breakeven now.

Wednesday, December 06, 2006

The Boston Strangle - from SFO mag

There is an interesting article in the Dec 06 edition of the SFO Mag on something called The Boston Strangle. Subscription is free.

I read the article initially and was graphing out the strangle playing with the numbers.

short 10x XEO 560 calls debit 15.6 each

short 10x XEO 580 puts debit 11.9 each

For more details and reasonings behind The Boston Strangle, you will have to subscribe and read the article ;-)

What I discovered was a discrepancy of the P/L if XEO expired at 558.8. The published P/L, $5380, and what's shown on my graph did not jive (I used thinkorswim). Not satisfied at such seemingly simple math, I graphed using Hoadley. TOS and Hoadley both showed $6300 profit.

A much more alert reader, Tom Opiela (photoman), pointed out where the problem is. A picture beats a thousand words. Click on pic to see full version.

I read the article initially and was graphing out the strangle playing with the numbers.

short 10x XEO 560 calls debit 15.6 each

short 10x XEO 580 puts debit 11.9 each

For more details and reasonings behind The Boston Strangle, you will have to subscribe and read the article ;-)

What I discovered was a discrepancy of the P/L if XEO expired at 558.8. The published P/L, $5380, and what's shown on my graph did not jive (I used thinkorswim). Not satisfied at such seemingly simple math, I graphed using Hoadley. TOS and Hoadley both showed $6300 profit.

A much more alert reader, Tom Opiela (photoman), pointed out where the problem is. A picture beats a thousand words. Click on pic to see full version.

Tuesday, December 05, 2006

20x INFY DEC 55 ATM puts, 10 days to expiration

Q:

I have 20x DEC 55 PUT bought at $1.25.. have only 10 days or so... need

some advice in terms of how to reduce the risk..bec. the stock is

already about $55.. should I close it.. or get some call to cover the

risk. Stock is up and down it was 52 three days back and now

55... stock pattern looks strong its going to swing based on the market..

but if u look at the PE its more than 46 times and doubled in last 4 month

after the split.

My thought when I bought the unit is to use the volatility to make some

money.. went to 55 from 53 in two days on average volume...

Would really appreciate any thoughts.

-------------------------------------------------------------------

A:

Time decay is against you in these last few days of the expiration cycle. At 20x u are losing roughly $90 per day just on time decay.

Time decay is against you in these last few days of the expiration cycle. At 20x u are losing roughly $90 per day just on time decay.

If stock stays above 55 by expiration u will lose the whole thing.

If you are long term bearish and must pick tops in rallies like this, at least buy longer term options where the time decay is dramatically slower. Look to jan or apr perhaps.

Here is the risk profile of your position, click on pic to see larger. See my video, how to read a risk graph if having trouble.

Here are some additional thoughts:

If the weather forecast is sunny, yet its actually starting to drizzle outside, which do you believe?

If the drizzle turns into light rain, what do you do?

If light rain persists for several hours, do you stick with the original sunny forecast or prepare accordingly when heading outside?

I have 20x DEC 55 PUT bought at $1.25.. have only 10 days or so... need

some advice in terms of how to reduce the risk..bec. the stock is

already about $55.. should I close it.. or get some call to cover the

risk. Stock is up and down it was 52 three days back and now

55... stock pattern looks strong its going to swing based on the market..

but if u look at the PE its more than 46 times and doubled in last 4 month

after the split.

My thought when I bought the unit is to use the volatility to make some

money.. went to 55 from 53 in two days on average volume...

Would really appreciate any thoughts.

-------------------------------------------------------------------

A:

Time decay is against you in these last few days of the expiration cycle. At 20x u are losing roughly $90 per day just on time decay.

Time decay is against you in these last few days of the expiration cycle. At 20x u are losing roughly $90 per day just on time decay.If stock stays above 55 by expiration u will lose the whole thing.

If you are long term bearish and must pick tops in rallies like this, at least buy longer term options where the time decay is dramatically slower. Look to jan or apr perhaps.

Here is the risk profile of your position, click on pic to see larger. See my video, how to read a risk graph if having trouble.

Here are some additional thoughts:

If the weather forecast is sunny, yet its actually starting to drizzle outside, which do you believe?

If the drizzle turns into light rain, what do you do?

If light rain persists for several hours, do you stick with the original sunny forecast or prepare accordingly when heading outside?

Monday, December 04, 2006

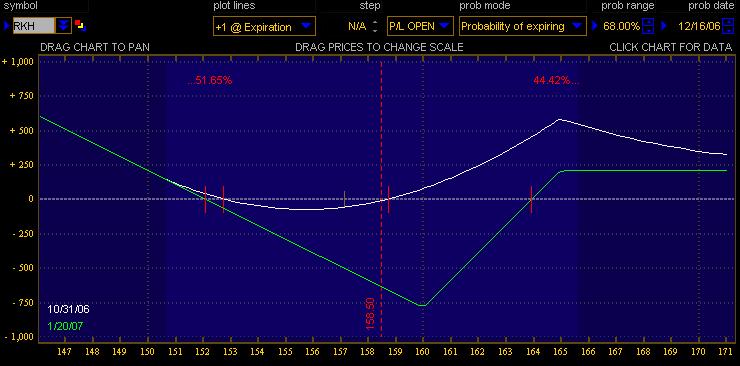

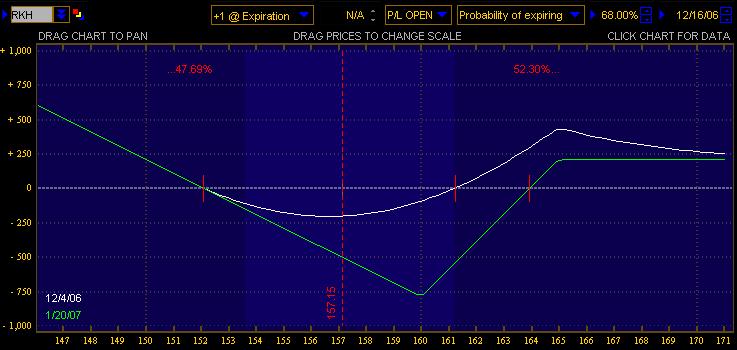

RKH ratio back spread

This question was originally posted on optionstradingcoach yahoo group.

------------------------------------------------------------------

Hello,

about 2 or 3 weeks ago I put on a ratio back spread on RKH. At that

time RKH was at around 158.50

So I sold 2 January 165 puts and bought 3 January 160 puts for a

credit of 2.10

A few days ago, with RKH at around 156, this position still had a

loss, if I had bought it back. Don't understand why, seeing that the

underlying had gone in the right direction more than 2 bucks.

Yesterday I got exercised on my short puts, so I then exited the

whole position, but the question remains.

Many thanks, gis

P.S. There is a chance that when I checked my position that I

actually made a mistake and I already had a profit, but am not sure.

P.P.S Sorry for not being able to provide more accurate numbers. I

need to improve my trading diary.

P.P.S The difference in IV when entering the spread was about 36 for

the long puts and 35 for the short puts, so don't think that was the

reason.

-------------------------------------------------------------------------

Hi gis, (click on pic to enlarge)

Here is your original risk profile, I estimated the entry date a few weeks back when u first put on the position. This is very much a long vega position with a large or quick move being the index sentiment.

Here is your original risk profile, I estimated the entry date a few weeks back when u first put on the position. This is very much a long vega position with a large or quick move being the index sentiment.

See my video "how to read a risk graph" if the pictures are gibberish to you.

Here is your risk profile today (assuming no assignment). Note the stock has not moved and decay is eating away at the white line.

Graphs created using Thinkorswim.

Frankly with the vol and price characteristics I would be inclined to do neutral calendars on this since it does not look like a mover to me.

------------------------------------------------------------------

Hello,

about 2 or 3 weeks ago I put on a ratio back spread on RKH. At that

time RKH was at around 158.50

So I sold 2 January 165 puts and bought 3 January 160 puts for a

credit of 2.10

A few days ago, with RKH at around 156, this position still had a

loss, if I had bought it back. Don't understand why, seeing that the

underlying had gone in the right direction more than 2 bucks.

Yesterday I got exercised on my short puts, so I then exited the

whole position, but the question remains.

Many thanks, gis

P.S. There is a chance that when I checked my position that I

actually made a mistake and I already had a profit, but am not sure.

P.P.S Sorry for not being able to provide more accurate numbers. I

need to improve my trading diary.

P.P.S The difference in IV when entering the spread was about 36 for

the long puts and 35 for the short puts, so don't think that was the

reason.

-------------------------------------------------------------------------

Hi gis, (click on pic to enlarge)

Here is your original risk profile, I estimated the entry date a few weeks back when u first put on the position. This is very much a long vega position with a large or quick move being the index sentiment.

Here is your original risk profile, I estimated the entry date a few weeks back when u first put on the position. This is very much a long vega position with a large or quick move being the index sentiment.See my video "how to read a risk graph" if the pictures are gibberish to you.

Here is your risk profile today (assuming no assignment). Note the stock has not moved and decay is eating away at the white line.

Graphs created using Thinkorswim.

Frankly with the vol and price characteristics I would be inclined to do neutral calendars on this since it does not look like a mover to me.

Sunday, December 03, 2006

Calendar spread pow wow tonite 12/4 at 8pm pacific

I am going to do a short, basic session on calendar spreads (15 to 20 min) then open up to questions.

The conference software will be www.yugma.com. Conference ID 83170611 or click here. No registration is necessary. There is a small java plug-in that gets installed automatically for the first time.

I am seeing that it works with IE better than Firefox. Two monitors are best, as u can maximize the shared desktop on one screen, and move the chat blocks onto another screen. Voice is done via conf call number shown on the top of the chat box. Long distance charge may apply. Not sure how skype would work in this case.

junky

lyn.express@gmail.com

skype: optionsjunky

Yahoo IM: optionsjunky

The conference software will be www.yugma.com. Conference ID 83170611 or click here. No registration is necessary. There is a small java plug-in that gets installed automatically for the first time.

I am seeing that it works with IE better than Firefox. Two monitors are best, as u can maximize the shared desktop on one screen, and move the chat blocks onto another screen. Voice is done via conf call number shown on the top of the chat box. Long distance charge may apply. Not sure how skype would work in this case.

junky

lyn.express@gmail.com

skype: optionsjunky

Yahoo IM: optionsjunky

Friday, December 01, 2006

Q:

Q:+ mar 75c -5.25 debit

- dec 75c +.75 credit

+ jan 80c -.85 debit

- mar 75c +5.0 credit

My bias is the stock (WLP goes back to 74 by expiration) What should I do?

A: this is not a great position to be in even if you are convinced the stock goes back to 74. The credit received for the dec 75c was small, offering the trader little buffer against an upside move. The upside jan 80c (protection) is a whopping 5 pts away. This position is also taking on hard delta, meaning the short is ITM and the delta growing more than 2x as fast as the long leg if this trend persists.

For 10 spreads if stock goes back towards 75 u have a chance to breakeven on the whole thing. But, if we expire at 80, $3k loss.

Not a great risk reward trade.

I would say if one is absolutely convinced at the 74 bias, at least reduce the position by 1/2 immediately. Ask yourself this question, If I had no position in WLP right now, would I short 340 shares of stock? (delta exposure of current position sized at 10 spreads).

Subscribe to:

Posts (Atom)