Here is a RUT IC posted by a fellow trader from

Advanced Options Strategies. Hi probability trade given the limited credit. I have asked for his exit/adj plans and will post details as I get them.

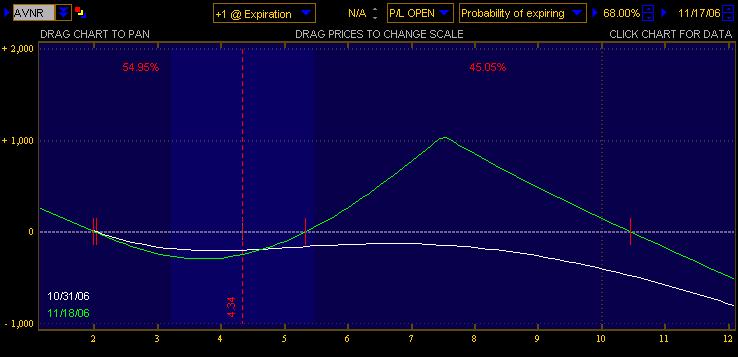

11/3/06

The trader added the nov 780/790c spared for .65 credit, citing multiple resistance zones between the current price and 780, with 780 being the last resistance point.

Note how the profit zone narrowed with this maneuver and risk is increased on the extreme upside.